Emissions Intensity – We’re On It

05 October 2021

The findings from the latest Intergovernmental Panel on Climate Change (IPCC) report, published recently, are sobering.

The past five years have been the hottest on record since 1850, the sea level rises we are seeing are now irreversible, and the authors believe that the Paris Agreement on climate change’s goal to keep the rise in global temperature under 1.5C will be reached in 2040 rather than 2050.

We are in a climate emergency. It has implications for every aspect of an organisation’s life: its culture, its communications and its activities.

Strong action is needed from business, and this includes, but goes far beyond, managing just operational emissions. In fact, in assessing a business’ climate response, emissions from its operations and its full value chain are important.

Last month, I explained that Mike Berners-Lee and his team at Small World Consulting are helping the University of Sheffield AMRC understand our carbon footprint and our low carbon transition. We have been using a framework Small World Consulting been developing to help us understand:

- to what extent is the AMRC pushing for the low-carbon transition that we need to see;

- to what extent is the AMRC well-positioned to thrive under such a transition.

Now, that assessment is in!

Over the last couple of months we’ve started to digest this information, think about where we go from here and, in the spirit of transparency, I wanted to share this information via my regular blogs. We’ll be using this assessment as our benchmark against all future assessments.

So where better to start than at the first of the eight criteria: Emissions intensity.

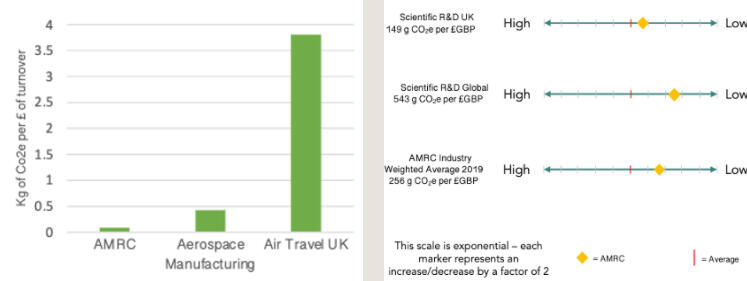

Emissions intensity is fundamentally asking How does the AMRC’s operational and upstream emissions intensity compare to its peer group, competition and substitutes?

Sounds straightforward but our first hurdle was data. Unfortunately, we didn’t have recent data from a standard current carbon audit (which I will address in next month’s blog) and so we were left trying to use the best data we had available: utility bills, travel costs and our purchase ledger.

From this data we were able to determine estimates for our Scope 1, Scope 2 and Scope 3 upstream emissions (see my “Finding a Mentor” blog for further explanation) which we then converted into grams of CO2e per £GBP of turnover.

And that gave us our first insight:

The AMRC’s operational and upstream emissions intensity of 83 gCO2e per £GBP of turnover.

It’s at this point that the voice of Hans Rosling screams in my head: “Never leave a number all by itself. Never believe that one number on its own can be meaningful. If you are offered one number, always ask for at least one more. Something to compare it with.”

And so we have compared ourselves from two perspectives: (i) against averages from other research organisations and the industries for which we carry out research, and (ii) selecting the aerospace sector, comparing ourselves to other important steps in the lifecycle (see images below).

What insights have we gained from our emissions intensity assessment and what actions are we taking?

Well, let’s start with the data problem. For the reasons set out above, we have a medium level of confidence in the emission intensity figures and so have commissioned a full carbon audit to be completed in September. Let’s see if it dramatically changes the position.

Secondly, our Scope 1 emissions (company facilities and company vehicles) are relatively low. Not a surprise given that we are a research organisation and over the past decade the AMRC has invested in many on site low carbon technologies such as wind power generation, ground source heat pumps and a small district heating system to reduce the amount of utilities we buy in.

Our Scope 3 upstream emissions (purchased goods and services, employee commuting etc) were relatively high and something we are looking to address further through discussions with our suppliers and through hybrid working as we come out of the Covid-19 pandemic. We have roughly 500 employees who were commuting to the AMRC prior to the pandemic and we will be piloting hybrid working arrangements from 6 September this year which we expect will have a positive impact on our Scope 3 upstream emissions.

Our Scope 2 emissions were a significant proportion of our total emissions (purchased utilities) and this is an area where we need to do more work. We need to improve the energy efficiency of our operations but currently don’t have the data granularity to categorically understand which parts of our operations need focus. We are currently installing sub-meters across the AMRC estate which we hope will be the first step on understanding the actions we need to take. We have already electrified a lot of our heat requirements but there’s still more work to do here.

Finally, the sector comparison gave us the strongest insight. It’s obvious but the data shone a bright light on the potential impact the innovation we deliver at the AMRC can have on upstream material selection, manufacturing processes and downstream in-use carbon emissions.

All this presented some tough questions.

We operate at any one time with roughly 600 live projects in the AMRC but how many are clearly contributing to the low carbon transition?

Do we run the risk of unintended consequences or rebound effects and if yes, what more can we do?

We are not alone in these considerations; I know many of our partners and collaborators are wrestling with the same questions. Which brings me back to why I started charting our sustainability journey in these blogs: to share what we have learned about ourselves, warts and all.

Collaboration has been a cornerstone of the AMRC’s success and part of that should be shared learning about how we operate as manufacturers.

We know we have work to do, but to recognise where that work needs to be done is a big stride down the road to sustainability.

Next month: Carbon Accounting Quality